The 50-Year Mortgage: Miracle or Mirage?

Introduction

Lately there’s been growing talk about introducing a 50-year mortgage as a way to make homeownership more “affordable.” On the surface, it sounds like a lifeline for first-time buyers priced out of the market, lower monthly payments, easier qualification, and longer repayment periods.

But when you look at the numbers, it becomes clear that the goal isn’t purely consumer relief, it’s also about stabilizing a housing market facing ongoing pressure.

Let’s unpack how a 50-year mortgage compares to the traditional 30-year loan, and what it really means for affordability in America.

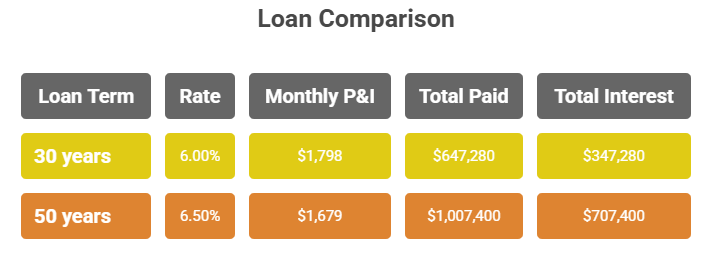

30-Year vs 50-Year: The Numbers Behind the Headlines

Scenario:

- Home price: $300,000

- 30-year fixed rate: 6.00%

- 50-year fixed rate: 6.50% (slightly higher due to longer risk)

- No taxes or insurance for simplicity

That’s a $119/month difference in payment, at the cost of doubling the lifetime interest and staying in debt 20 extra years.

The “affordability” gain here is a mirage. It lowers the monthly figure just enough to maintain home prices, while locking the borrower into near-perpetual debt.

The Real Goal Behind the 50-Year Mortgage

🏦 1. To Sustain Current Home Values Without Addressing Supply

A 50-year term doesn’t create more homes, it simply expands the buyer’s ability to borrow more over a longer period. That, in turn, allows prices to remain at current levels rather than adjusting downward through natural market forces.

💰 2. To Extend Interest Revenue for Lenders

The average borrower pays mostly interest during the first 10–15 years of a mortgage. By extending the term to 50 years, banks ensure decades more interest income, even if you sell or refinance early.

🧩 3. To Act as a Pressure Valve for a Heavily Strained System

With high rates and stagnant wages, many Americans are already priced out. Instead of addressing those root problems, policymakers are quietly saying:

“We can’t raise wages or lower prices — so we’ll just make you pay longer.”

🏠 4. To Normalize Perpetual Debt

The 50-year term begins to blur the line between mortgage and lifelong financial obligation. It’s less about ownership and more about debt maintenance, resembling models seen in heavily financialized economies.

In many developed nations, from the U.K. and Canada to Australia, we’ve seen what happens when housing becomes more of a financial asset than a place to live. The U.S. is now showing similar patterns, with policies increasingly focused on sustaining asset values rather than restoring affordability.

⚙️ 5. To Offer Political Optics, Not Real Relief

It’s an easy talking point: “We’re helping Americans buy homes.” But the fine print shows that most buyers save little each month, while lenders collect double in interest over time.

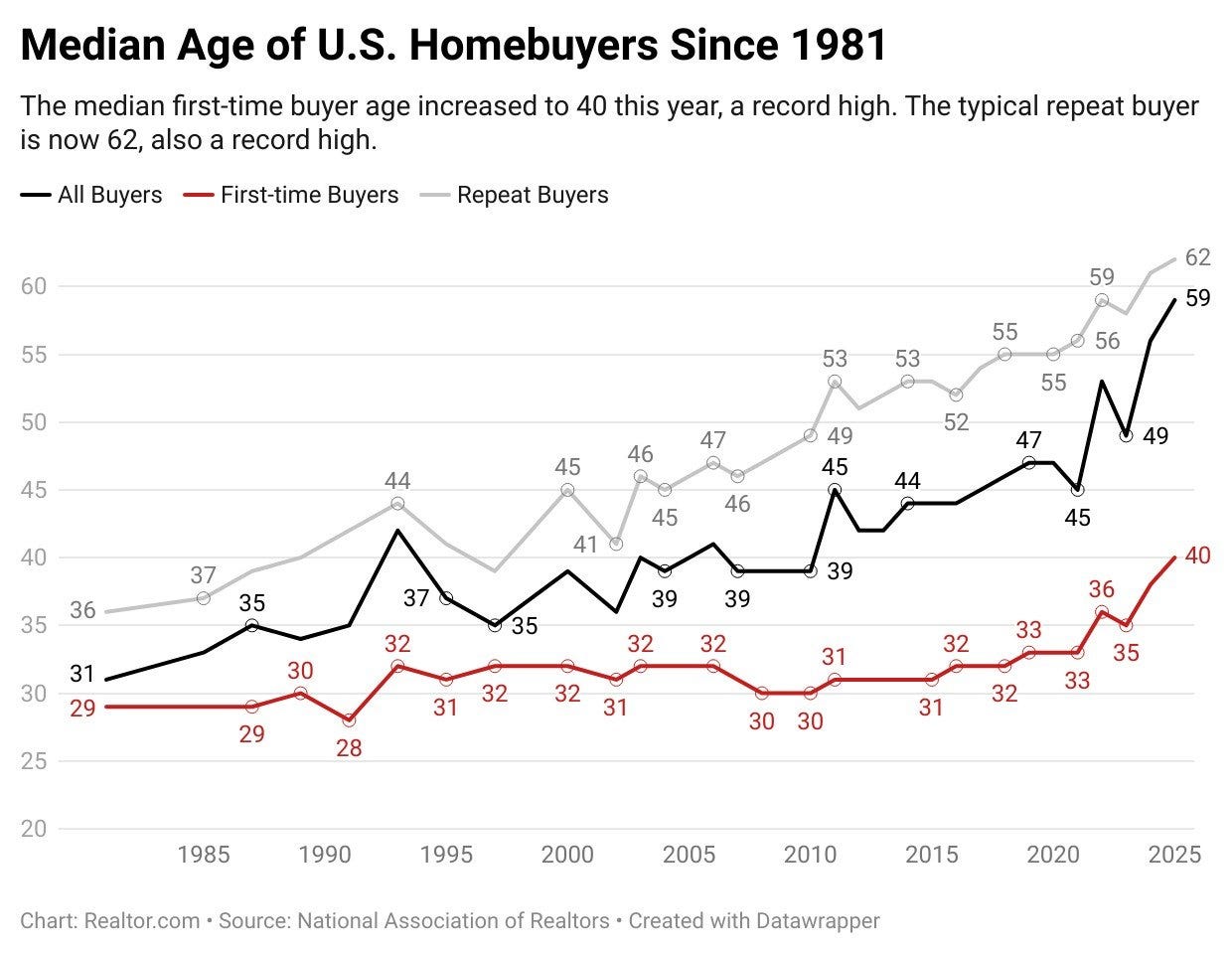

The Real Problem: Affordability and a Shifting Buyer Profile

According to the 2025 NAR Profile of Home Buyers and Sellers, housing affordability, not lack of demand, is what’s reshaping who can buy a home:

- First-time buyers now make up just 21% of the market, the lowest share in history (the norm before 2008 was ~40%)

- The median age of a first-time buyer is now 40, compared to the late 20s in the 1980s

- The median down payment has climbed to 10%, the highest since 1989

- High rent, student debt, and childcare costs are the top barriers to saving

This isn’t a generation uninterested in buying, it’s one systematically priced out. Extending mortgages to 50 years won’t fix that; it just masks the real issue while preserving inflated asset values.

Real-World Solutions to Housing Affordability

If we truly want to make homeownership attainable again, we have to target the root causes. not the symptoms.

1. Expand Housing Supply

Encourage zoning reform, streamline permitting, and incentivize smaller-footprint homes, ADUs, and infill projects. You can’t lower prices without increasing inventory.

2. Strengthen First-Time Buyer Programs

Down-payment assistance, tax credits, and employer-based home savings programs directly help new buyers enter the market rather than stretching loan terms.

3. Realign Wages and Home Prices

Decades of stagnant wage growth paired with runaway home appreciation have broken the balance. Wage policy, tax fairness, and curbing speculative investment by large corporations into single family housing are key to restoring that alignment.

As I discussed in a previous post, How Wealth Inequality and Wage Stagnation Broke the Housing Market, real wages have lagged far behind home price growth for decades. That gap is the root cause of today’s affordability crisis, and it’s the very reason proposals like a 50-year mortgage even exist.

4. Reinforce Local Communities

Investing in infrastructure, public transit, and broadband in smaller towns and rural regions (like many in Tennessee) can make more affordable areas viable for buyers priced out of urban cores.

Why It Matters

The housing market’s trajectory isn’t just an economic issue, it’s generational. The typical first-time buyer now enters the market more than a decade later than their parents did, often with higher debt and fewer assets.

A 50-year mortgage may sound like progress, but it’s ultimately a symptom of a deeper problem: the erosion of true affordability. If we want housing to be a path to stability and wealth, not a lifelong liability, the goal shouldn’t be to make debt last longer. It should be to make homeownership possible within the timeframes that once built the American middle class.

Final Thoughts

A longer loan term can make a spreadsheet look better, but it doesn’t solve the fundamental equation: too few homes, too much debt, and too little income growth.

The answer isn’t a 50-year mortgage, it’s restoring the conditions where a 30-year mortgage feels realistic again.

Elevate Your Career

Learn how you can thrive in our brokerage. Contact us for more info!